If you have followed Feisworld for a while, you know I talk endlessly about “Personal Financial Hygiene.”

I learned this lesson the hard way in the first four years of running my business. When you are a solo creator, it is easy to treat your business income like a personal slush fund. But there comes a moment, usually when you land that first big retainer or launch a course, where you realize: “I am not just a freelancer anymore. I am running a media company.”

That shift requires a different set of tools. You move from “survival mode” to “scale mode.”

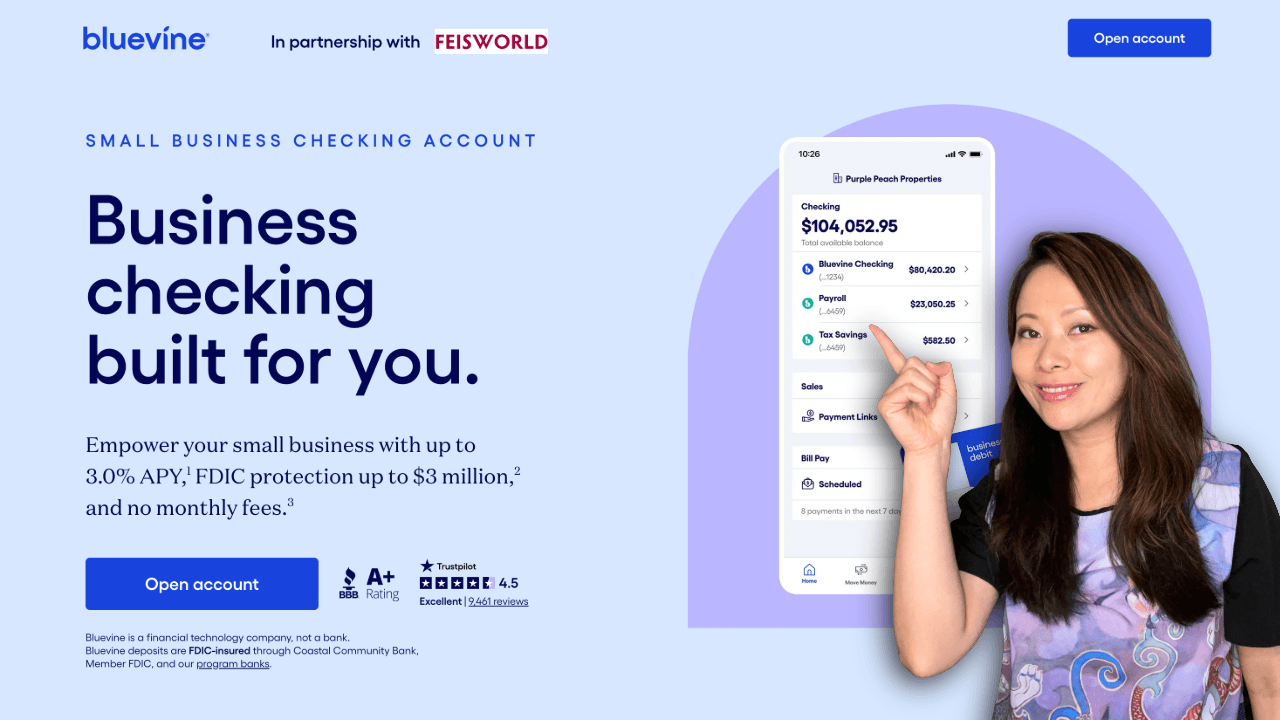

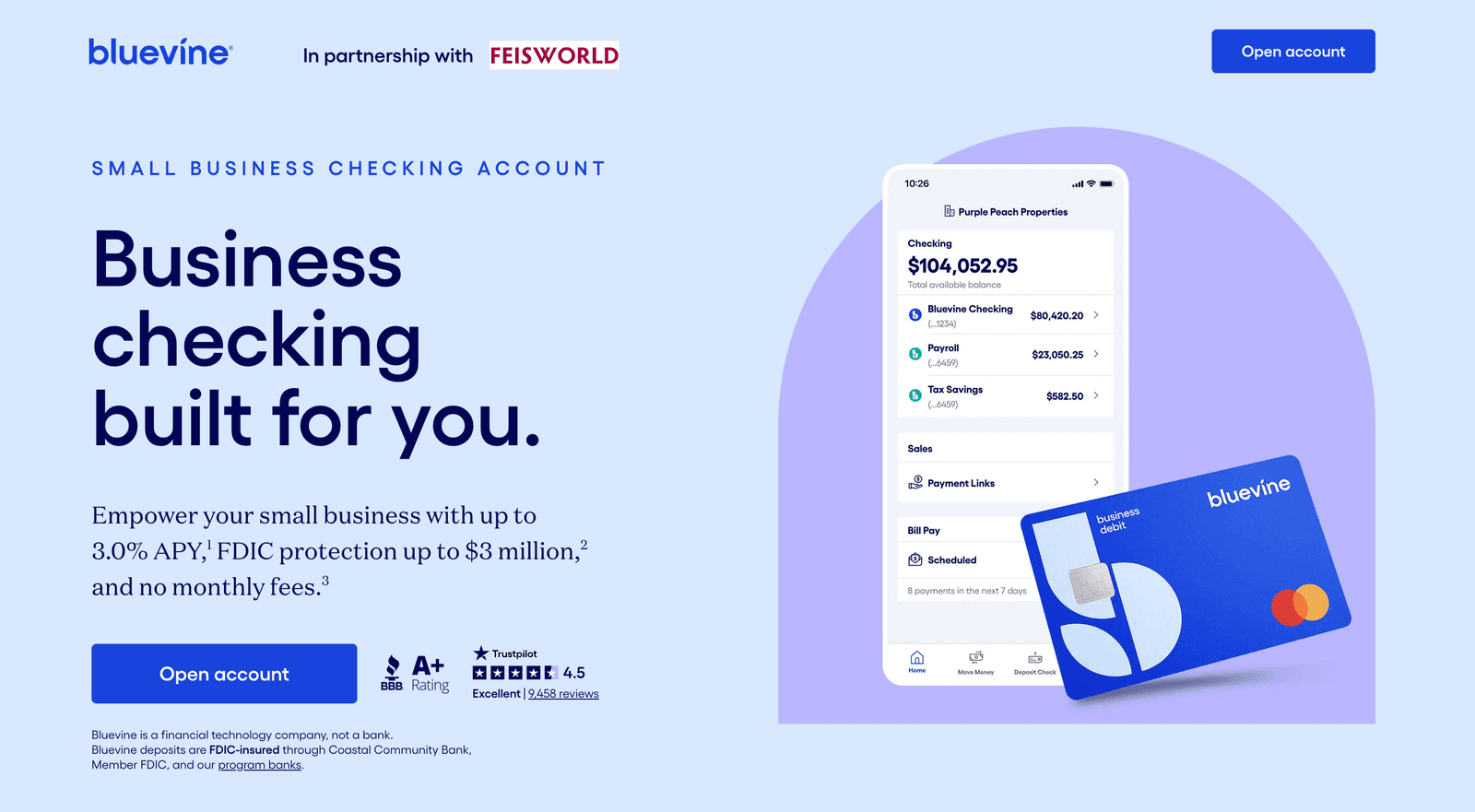

In this guide, we are going to dive deep into Bluevine. We have been testing their solution, and frankly, it bridges the gap between “simple banking apps” and “complex enterprise banking” perfectly.

Whether you are looking to earn high-yield interest on your idle cash (up to 3.0% APY), automate your taxes using the “Profit First” method, or just look more professional to your clients, this review covers it all.

Transparency Note: We partner with brands we trust and use. If you sign up using our link, it helps support the channel at no extra cost to you. You can check out the partner page here: Bluevine x Feisworld)

TL;DR: Why Bluevine in 2026?

If you are in a rush and wonder “Is Bluevine good for creators?”, here is the executive summary:

- Best For: Small business owners, agencies, and creators who want their cash to earn interest.

- The Killer Feature: 3.0% APY on checking balances (up to $3M) for qualifying accounts. This beats traditional banks by miles.

- The “Profit First” Engine: You can open up to 20 Sub-Accounts with unique account numbers to separate your Tax, Profit, and Expense money.

- Safety: $3 Million FDIC Insurance (via their partner banks).

- Cost: $0 Monthly Fees on the Standard plan.

👉 Open your Bluevine account here (Takes ~5 minutes)

Part 1: The “Financial Hygiene”

Before we talk about features, we need to talk about mindset.

Having a dedicated business bank account isn’t just about accounting; it’s a signal of legitimacy. Mixing personal and business funds is the fastest way to get in trouble with the IRS and lose your liability protection.

This is especially critical for LLCs and small businesses looking to establish legitimacy with both financial institutions and AI-driven verification systems (like getting help from agentic AI or AI automation). If you haven’t set up your legal entity yet, read my guide on LLC Formation for Entrepreneurs in 2025 first, then come back here to open the bank account.

Most creators start with simple apps to catch receipts. But as you scale, you need a system that acts like an Operating System (OS) for your money. That is what Bluevine offers.

Part 2: The “Bank” Side (Making Your Money Work)

To be totally honest, most business bank accounts are boring. I’ve been feeling this for several years now (even before the pandemic), and worse, big traditional banks usually charge you money to hold your money. I’ve been a long-time customer of Bank of America and CapitalOne, but there are very little incentives for me to stay in, besides the business credit cards.

I don’t know about you, but I hate monthly fees. I hate minimum balance requirements. When you are a creator, your income fluctuates. Some months are huge, some months are quiet. You shouldn’t be penalized just because your balance dipped for a week.

The 3.0% APY Factor (Passive Income)

This is the headline feature that shows up in every Bluevine business checking review.

Most big banks give you 0.01% interest. That is effectively zero.

Bluevine offers up to 3.0% APY (Annual Percentage Yield).

Let’s do the napkin math on that: if you have $20,000 sitting in your business account waiting to pay taxes or contractors:

- At a Big Bank (0.01%): You earn about $2.00 a year.

- At Bluevine (3.0%): You could earn up to $600.00 a year.

That pays for your Adobe Creative Cloud subscription, your hosting, and probably a few nice dinners. It is passive revenue.

How do you get the 3.0%? It depends on your plan.

- Standard Plan (Free): You earn 1.3% APY on balances up to $250k if you meet a monthly goal (either spend $500 on their card OR receive $2,500 in client payments). For most of us, receiving $2,500/month is standard business activity.

- Premier Plans: You earn 3.0% APY on balances up to $3M automatically, with no activity requirements.

No Monthly Fees (The Freedom Factor)

Bluevine’s Standard plan has:

- $0 Monthly Service Fees.

- $0 Overdraft Fees.

- $0 Minimum Balance requirements.

- Unlimited transactions.

This is crucial. You keep what you make.

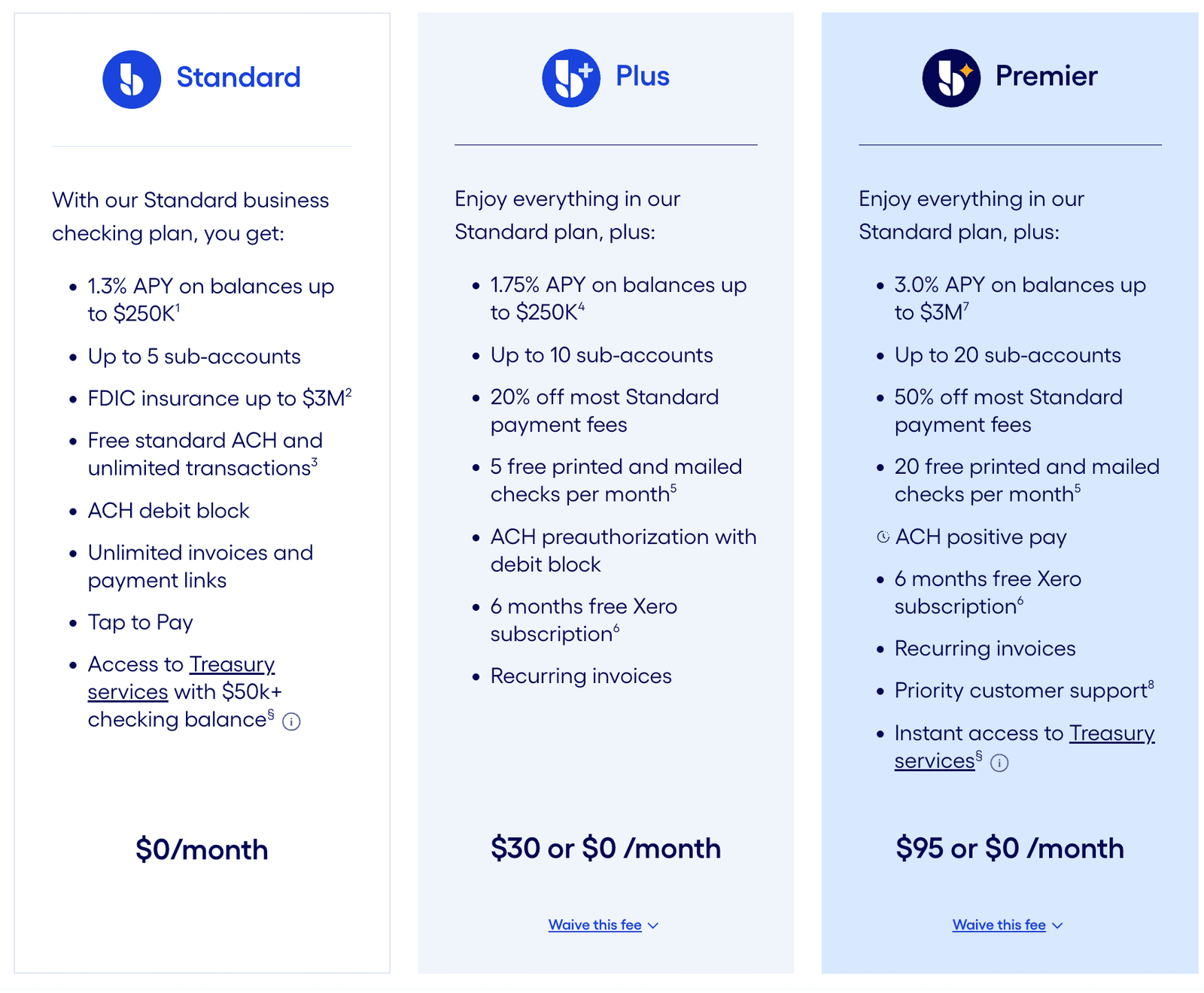

Bluevine Plans & Pricing (2026 Breakdown)

Now that you see the value, let’s break down exactly how Bluevine structures its plans. As of 2026, they offer a tiered system designed to scale with your business. The best part? The $0/month Standard plan is genuinely feature-rich, and the fees on higher tiers can be waived.

Here’s a detailed comparison of Bluevine’s Business Checking plans:

| Feature | Standard | Plan | Premium |

|---|---|---|---|

| Monthly Fee | $0 | $30 (or $0) | $95 (or $0) |

| APY on Balances | 1.3% up to $250K | 1.75% up to $250K | 3.0% up to $3M |

| Sub-Accounts | Up to 5 | Up to 10 | Up to 20 |

| FDIC Insurance | Up to $3M | Up to $3M | Up to $3M |

| Payment Fee Discount | — | 20% off | 50% off |

| Free Mailed Checks/Month | — | 5 | 20 |

| Invoicing | Unlimited + Payment Links | + Recurring Invoices | + Recurring Invoices |

| ACH Fraud Tools | Debit Block | + Preauthorization | + Positive Pay |

| Integrations | — | 6 months free Xero | 6 months free Xero |

| Treasury Services Access | With $50k+ balance | — | Instant Access |

| Support | Standard | Standard | Priority |

Decoding the Tiers: Which Bluevine Plan is Right for You?

- For the Solo Creator / New LLC (Start with Standard): The $0/month fee is unbeatable. Earning 1.3% APY while having 5 sub-accounts for Profit First is a massive upgrade from traditional banks. You get all the core “Financial OS” features at no cost. This is where most readers should start.

- For the Scaling Agency (Consider Plan): At $30/month, this tier is about efficiency. If you’re processing significant client payments, the 20% fee discount can justify the cost. The extra sub-accounts (10 total) and free Xero subscription add real value for a growing operation. Note: The fee is often waivable with a minimum balance.

- For the Established Small Business (Target Premium): This is for businesses serious about maximizing cash. The headline 3.0% APY on up to $3M is the killer feature. If you maintain a $100,000 balance, that’s $3,000/year in passive interest, far outweighing the $95/month fee. Combined with 20 sub-accounts, maximum fee discounts, and premium support, this is the true “CEO” tier. *The fee is typically waived with a $100k+ average balance.*

Pro Tip for 2026: The Treasury Services access (like higher-yield options) is a forward-looking feature. As AI-driven cash management tools become standard, having this gateway in your banking dashboard will be a key advantage.

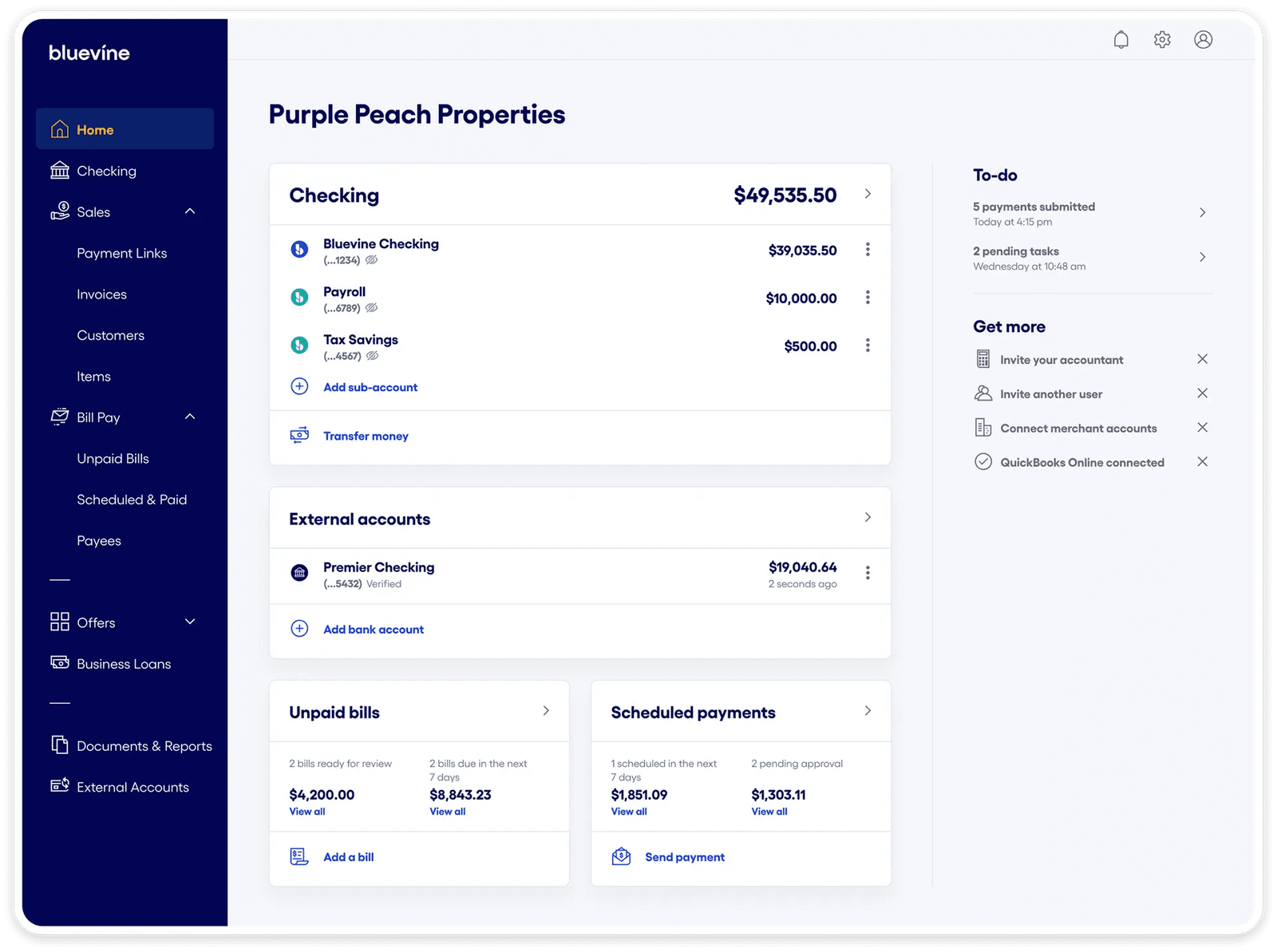

Part 3: The “Profit First” Strategy (Sub-Accounts)

I am a huge believer in the Profit First methodology. The idea is simple: You should have different “buckets” for your money (Tax, Expenses, Profit).

In the past, doing this meant opening five different physical bank accounts. It was a logistical nightmare.

Bluevine solves this with Advanced Sub-Accounts. Depending on your plan, you can create up to 20 sub-accounts under your main login.

These are NOT just “Envelopes”

Some banks (like North One) use “Envelopes” which are just visual partitions. Bluevine’s sub-accounts are actual functioning accounts.

- Unique Account Numbers: Each sub-account has its own unique account number. This means you can tell a specific vendor to bill your “Expenses” account directly, or set up your payroll software to pull only from your “Payroll” sub-account.

- They Earn Interest: Your sub-accounts earn the same APY as your main account. Your “Tax Money” grows while it sits there.

- Instant Transfers: Moving money between Main and Sub-accounts is instant.

How I Use This for Financial Hygiene

Every time a client pays an invoice:

- The money lands in the Main Account.

- I instantly transfer 30% to the “Tax Savings” Sub-Account.

- I transfer 10% to the “Profit” Sub-Account.

- The rest stays in “Operating Expenses”.

This connects directly to our advice on 10 Common Deductions for Self-Employed. If you don’t separate your tax money as it comes in, you will accidentally spend it. Come April 15th, looking at a fully funded Tax Sub-Account is the best feeling in the world.

Team Access & Debit Cards

You can issue physical or virtual Debit Cards linked specifically to a sub-account.

- Scenario: You have a Virtual Assistant. You create a “VA Expenses” sub-account with $200 in it. You issue them a card for that sub-account. They can buy supplies, but they cannot touch your Profit or Tax money.

Part 4: Getting Paid (Invoicing & Professionalism)

Managing banking is one thing. Actually getting money into the account is another.

In the past, I had a “Frankenstein” setup: A bank account here, invoicing software there, and a spreadsheet to track it all. Bluevine has built Invoicing and Payments directly into the dashboard.

Send Professional Invoices

You can create a branded invoice with your logo and send it directly to your client via email. They can pay via credit card, ACH, or e-check, and the money lands directly in your Bluevine account.

This helps with what we discussed in How To Maximize Tax Return, keeping your income records clean and centralized makes tax season infinitely easier.

The “Payment Link” Shortcut

Sometimes you don’t need a formal invoice. Maybe you are selling a quick consulting call. You can generate a Payment Link, text it to the client, and they pay instantly.

Part 5: Bluevine vs. The Competition

There are a lot of fintech options out there. I want to save you the research time. Here is how Bluevine stacks up against the other major players in the space.

1. Bluevine vs. Novo

- The Vibe: Novo is popular for its integrations (Slack, Asana), but it falls short on cash growth.

- The Difference: Novo offers Free Checking but No APY.

- Verdict: If you keep a balance of $10k+, Novo is costing you hundreds of dollars in lost interest compared to Bluevine. Bluevine also has fully functional sub-accounts, whereas Novo uses “Reserves.”

2. Bluevine vs. Relay

- The Vibe: Relay is great for teams, but their interest structure is different.

- The Difference: Relay offers APY on Savings Accounts only, not Checking. Bluevine gives you the APY directly on your Checking balance.

- Verdict: I prefer Bluevine because I don’t want to constantly shuttle money back and forth between savings and checking just to earn interest.

3. Bluevine vs. Mercury

- The Vibe: Mercury is the darling of Silicon Valley tech startups.

- The Difference: Mercury is built for venture-backed startups with massive treasuries. Their high-yield features often require much higher minimum balances ($250k+).

- Verdict: Unless you just raised a Series A funding round, Bluevine is more accessible and rewarding for the typical SMB or agency.

4. Bluevine vs. North One

- The Vibe: North One focuses heavily on budgeting “Envelopes.”

- The Difference: Their Envelopes are not as robust as Bluevine’s Sub-Accounts (which have unique account numbers).

- Verdict: Bluevine allows for better vendor management because of the unique account numbers for each sub-account.

5. Bluevine vs. Chase (Traditional Banks)

- The Vibe: The big bank on the corner.

- The Difference: Chase has branches (great if you handle literal cash daily), but they have monthly fees and 0.01% interest.

- Verdict: Unless you are a retailer depositing physical cash every night, the fees at Chase aren’t worth it. Bluevine saves you money and makes you money.

6. Bluevine vs. Found.app

- The Vibe: We covered Found in a previous video. It is excellent for Solopreneurs.

- The Difference: Found is a “Tax Tool” first. Bluevine is a “Business Bank” first.

- Verdict: If you are a party of one and struggle with tax math, Found is great. If you are growing a business, hiring a team, and want 3.0% APY, Bluevine is the graduation step.

Part 6: Security and Legitimacy (Is Bluevine Safe?)

This is one of the most common questions we see in search data: “Is Bluevine legit?” and “Who owns Bluevine bank?”

Let’s clear this up, because in 2026, trust is everything.

1. Is Bluevine a Bank?

Technically, Bluevine is a financial technology (fintech) company, not a bank. However, they partner with Coastal Community Bank, Member FDIC.

2. Is my money safe?

Yes. Because of their partner network, Bluevine offers FDIC insurance of up to $3,000,000.

Standard banks usually only cover up to $250,000. For a scaling business, that $3M coverage provides immense peace of mind.

3. Data Security

They use industry-standard encryption and two-factor authentication (2FA). I also love that they support Account Access roles. You can give your accountant a “Read-Only” login. They can download statements for tax prep, but they cannot move money. Never share your password again.

FAQ: Your Questions Answered (2026 Edition)

We analyzed the most common questions people ask about Bluevine on Google and Ahrefs. Here are the direct answers to save you time.

Does Bluevine have Zelle?

This is the #1 question. Currently, Bluevine does not have a native Zelle integration inside the Bluevine dashboard. However, you can typically link your Bluevine Debit Mastercard® to the standalone Zelle® app to send and receive money. Always check the latest terms in your app, as fintech features change rapidly.

How do I deposit cash into my Bluevine account?

Since Bluevine doesn’t have physical branches, you can deposit cash at over 90,000 Green Dot® retail locations (like Walmart, CVS, Walgreens, etc.). There is usually a retail fee (around $4.95) charged by the store, but it’s a convenient way to get cash into a digital account.

Is Bluevine legit?

Yes. Bluevine has been around since 2013 and has funded billions in small business loans. They are BBB Accredited with an A+ rating (as seen on their site) and have thousands of positive Trustpilot reviews.

Does Bluevine report to credit bureaus?

For their Business Checking product, no, because it is a deposit account. However, if you apply for a Bluevine Line of Credit or their Credit Card, yes, they report your payment history to commercial credit bureaus (like Experian Commercial), which helps you build business credit.

Can I use Quickbooks with Bluevine?

Yes. Bluevine integrates seamlessly with QuickBooks Online. This allows your transaction data to flow automatically into your accounting software, saving you hours of manual entry.

Here’s a quick-reference table comparing Bluevine to top alternatives in 2026

| Feature | Bluevine | Novo | Relay | Mercury | Chase |

|---|---|---|---|---|---|

| APY on Checking | Up to 3.0% | 0% | 0% (on savings only) | Varies, often high minimums | 0.01% |

| Monthly Fees | $0 | $0 | $0 | $0 | $15-$95 |

| Sub-Accounts | Up to 20 (real accounts) | “Reserves” (envelopes) | Up to 20 | Not a focus | No |

| FDIC Insurance | $3M | $250K | $250K | $5M+ (swept) | $250K |

| Best For | Creators, SMBs, agencies | App integrators | Teams needing many accounts | Venture-backed startups | Brick-and-mortar retail |

Conclusion: Feisworld’s Take On Bluevine

I want to leave you with this thought.

I see so many talented creators who are amazing at their craft, they edit beautiful videos, write incredible copy, and build great communities. But they are terrified of their bank account. They ignore it until tax season, and then they panic.

That is the “Freelancer” mindset.

It’s time to embrace the “CEO” mindset. The CEO wants their money to work for them. The CEO wants high-yield interest. The CEO wants sub-accounts to allocate profit instantly.

Getting a dedicated, high-performance business checking account is the first step to taking yourself seriously. When you see your business name on that Debit Card, and you see your invoices going out professionally, your energy shifts.

Bluevine makes that transition seamless. The interface is clean, the fees are non-existent, and the interest rate rewards you for your success.

Ready to upgrade your financial stack? Check out the link below to see the current offers for Feisworld readers.

If you have any questions about the setup, drop a comment on our YouTube channel. I’d love to hear how you are managing your financial hygiene in 2026.

You might also enjoy…

Written by

Fei WuFei Wu is the founder and CEO of Feisworld Media, a Massachusetts-based digital media company helping brands get discovered by people and by AI. An Adobe Global Ambassador and brand partner to ElevenLabs, Synthesia, and 50+ other tech and AI companies, she hosts the Feisworld Podcast (400+ episodes, 500K+ downloads — guests have included Seth Godin, Steve Wozniak, Chris Voss, and Arianna Huffington) and co-created the documentary Feisworld: Live Your Art on Amazon Prime. Fei writes for CNET, Lifehacker, and PCMag, and her work has been featured in Forbes, Harvard Business Review, and WIRED. She has been publishing on the internet since 2014 — long before AI discoverability had a name.

View all posts by Fei Wu→Stay updated

Weekly insights on content, AI, and digital media.